How VOP and consumer awareness can help prevent APP fraud

The role of consumer awareness in fraud prevention

In April, the European Banking Authority (EBA) released an opinion highlighting the positive impact of PSD2 security measures, including strong customer authentication, across the European Union.

The EBA noted that these requirements have been effective in preventing fraud based on stolen credentials. However, fraudsters are adapting their techniques, and the EBA says that this is leading to a rise in more complex fraud types, particularly those involving social engineering.

Although it’s primarily the responsibility of banks to implement safeguards against and prevent fraud, consumers also have a role to play, particularly when social engineering is involved.

Consumer awareness and detecting fraud

Consumer awareness is arguably the first line of defence against financial crime. An informed consumer is a cautious one, and financial institutions, regulatory bodies, and law enforcement have all recognised the importance of educating consumers to prevent common digital payment mistakes and scams, including:

Overlooking recipient details

Perhaps the most mistake is not verifying recipient details carefully before authorising a payment. This can result in money going to fraudulent accounts. Many consumers don’t double-check account numbers or sort codes. They might also fail to confirm that the recipient’s name matches the account. Even small differences in email addresses or phone numbers tied to the payment can be a warning sign, but they often get missed.

Rushing transactions

Scammers often use urgency to trick consumers into making quick decisions. In the rush, many authorise payments without verifying if the request is legitimate. Warning signs get ignored, especially when someone feels pressured to act fast. Consulting with a trusted source or financial institution before making a significant transfer can prevent costly mistakes, but it’s often skipped.

Trusting unsolicited communications

People often trust unsolicited messages or calls that appear to be from a credible source. This can lead to sharing sensitive information with scammers or transferring funds to supposed “secure” accounts. Clicking on links in these messages often leads to fake payment sites, putting financial information at risk.

The role of Verification Of Payee in fraud prevention

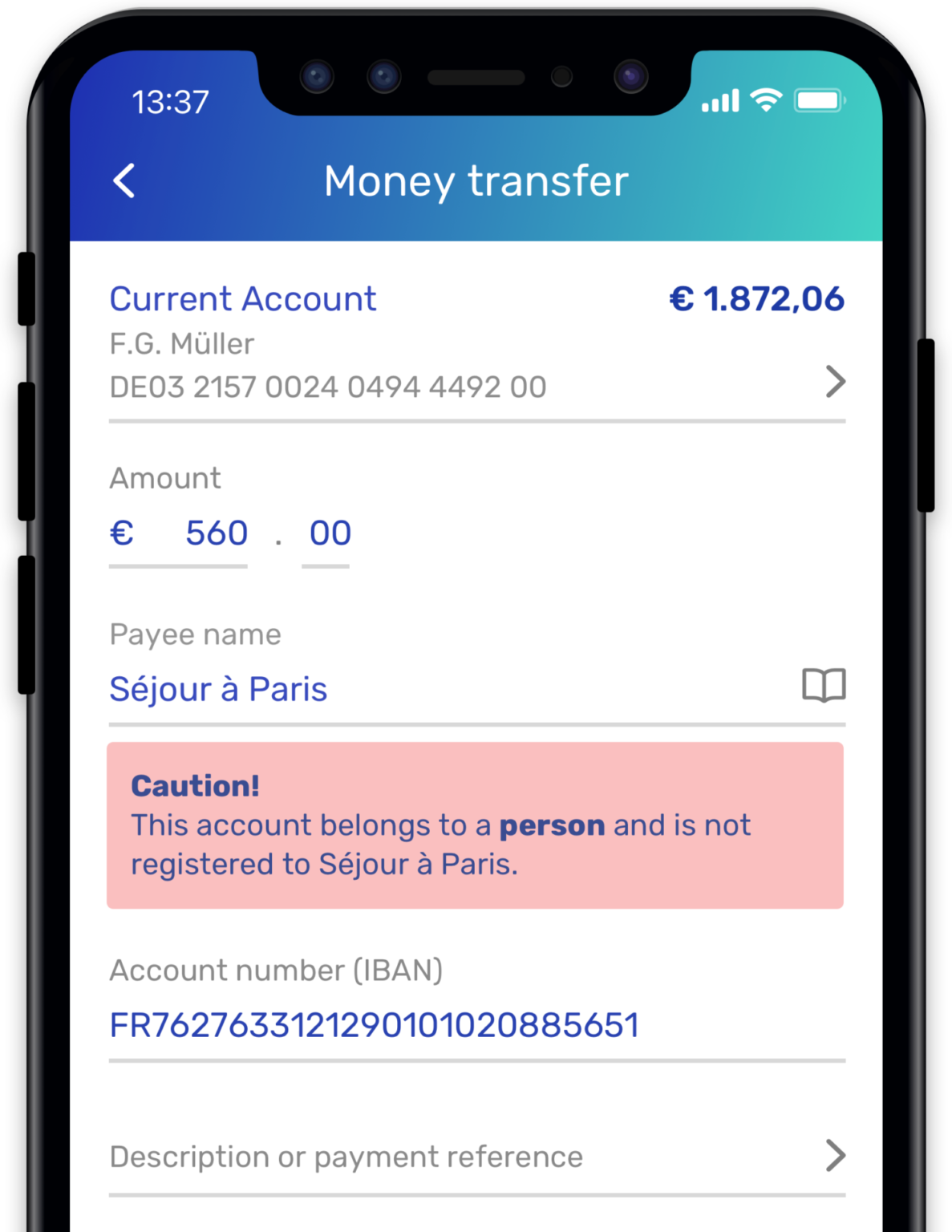

Verification Of Payee (VOP), also known as Confirmation of Payee (CoP) is a critical security measure designed to help consumers ensure they’re sending money to the intended recipient.

Essentially a name-checking service, VOP verifies that the account details that consumers enter when making a payment match those held by the recipient’s bank. It’s a relatively simple idea that’s playing a huge role in preventing payment errors and reducing the risk of falling victim to certain types of fraud, such as Authorised Push Payment (APP) scams.

The VOP process involves three key steps:

- Initiation of payment: The sender begins the process of making a bank transfer through their chosen payment channel (e.g., online banking, mobile app).

- Entry of payee details: The sender enters the payee’s details, including account name and number (IBAN). Some jurisdictions require additional details such as a sort code.

- VOP request: The payee’s bank checks the provided information against their records and generates a response based on the matching results. This is done within three seconds and presents the VOP results to the sender.

Although banks are ultimately responsible for implementing Verification Of Payee and sending alerts, it’s important that consumers double check and verify payee details as a first line of defence against fraud.

Depending on the VOP results, the sender will be presented with one of the following outcomes:

What this means | What to do | |

Exact match | The provided payee information matches the recipient’s bank records. | Proceed with the payment. |

Close match | Minor discrepancies between the provided information and the bank records. | Double check payee details before sending the payment. |

No match | The provided payee information does not match the bank records. | Do not send the payment until the payee can be verified. Contact the bank. |

Unavailable | The recipient’s bank doesn’t support VOP or cannot perform the verification. | Proceed with caution and attempt to verify the payee via other means. |

The role of banks in educating customers

Banks are not only responsible for implementing safeguards like VOP but also educating their customers about VOP and how it helps prevent fraud.

Banks should use multiple channels to share this information. In-app notifications and banners, for example, can provide real-time prompts during transactions while email campaigns and SMS alerts are effective for sending reminders and tips.

Regardless of how it’s delivered, messaging should be:

- Simple: Simplify VOP and fraud prevention by using plain language. Break down complex terms into everyday words. Analogies and real-life examples can make the concepts easier to understand. Avoid banking jargon and acronyms whenever possible to keep the message accessible.

- Consistent: Ensure clear and consistent communication across all platforms. Create a glossary of VOP-related terms with straightforward explanations. Customer service staff should be trained to use these simplified terms. Regularly update customer-facing materials to ensure they are clear and consistent.

- Engaging: Interactive tools can boost customer engagement. A VOP simulator could, for example, let customers practice in a safe environment while a VOP challenge game, where customers identify potential fraud risks, could reward accuracy and improve awareness.

As technology advances, VOP education will become more important. It’ll also become easier to deliver, with the use of AI enabling banks to provide real-time guidance based on user behaviour and suspicious transactions. Personalised fraud prevention advice, tailored to each customer’s habits and history, will also help make tips more relevant and effective.

We’re all responsible for fighting fraud

Verification Of Payee helps secure digital payments by reducing fraud and preventing misdirected transactions. For it to work well, banks and customers need to work together. Banks and financial institutions must make sure VOP systems are accurate, easy to understand, and reliable. They should also guide customers on how to interpret VOP results.

Customers play their part by staying alert, double-checking payee details, and understanding VOP alerts like “Close Match” or “No Match” before confirming a payment. With instant payments becoming standard, this shared effort is key to promoting a safer and more reliable financial system.

Want to know more?

Best in class Verification Of Payee solution

Schedule a meeting today

We are here to help answer any questions you may have about Verification Of Payee and the Instant Payments regulation.

The latest developments

The Digital Euro Is Coming, and Consumers Will Expect to Know Who They’re Paying

There’s something about Canada

6 Things We Took Away from Nacha Smarter Faster Payments

Scammers target Dutch taxpayers as the Belastingdienst bank switch creates new fraud risk

The most important decision in Nordic payments isn’t about the rails.