Get the answers you need to move forward with confidence.

General questions

On the bank’s side, there are two important things to consider.

First of all, the API that allows for Account Name Verification has to be integrated into your online banking environment.

Secondly, data provisioning has to be taken care of. This concerns the provisioning of customer data by your bank to SurePay so that SurePay’s algorithm can match the payment data to your bank’s customer data. Further information on required implementation efforts can be found in the sample Implementation Plan

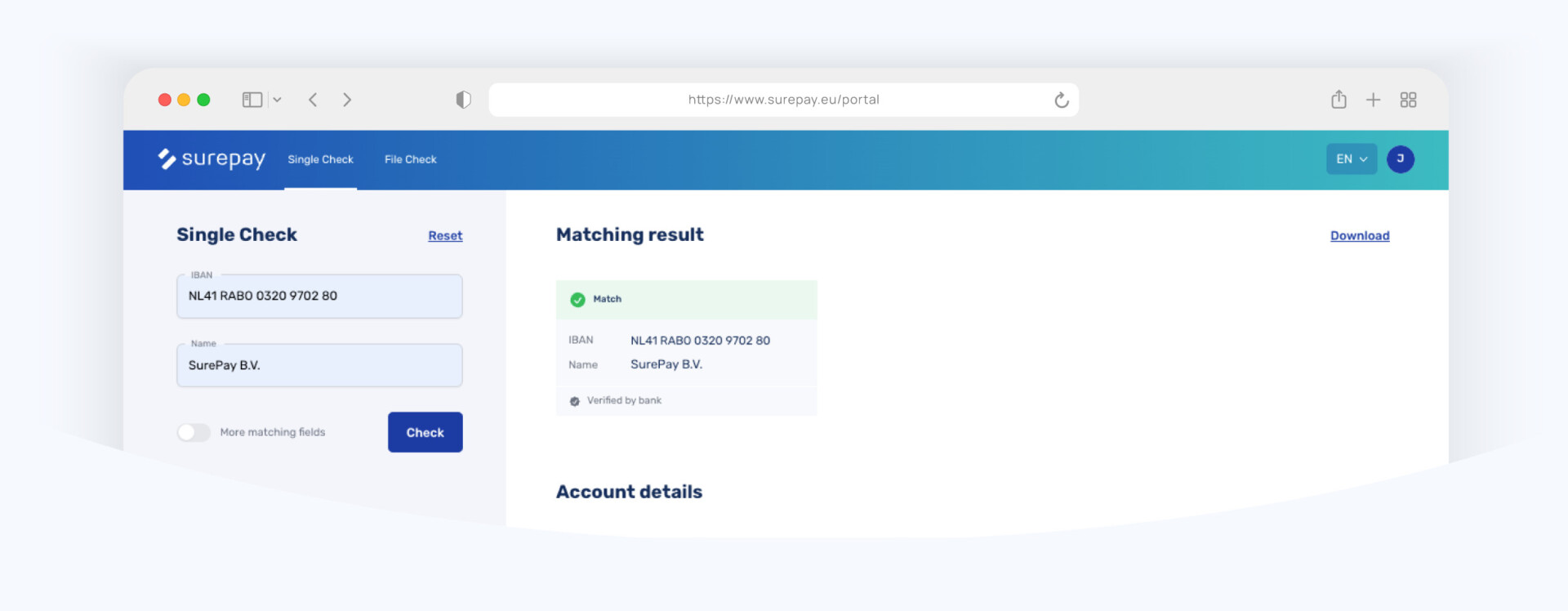

When making a transfer online, Verification Of Payee, the IBAN-Name Check and the SurePay Confirmation of Payee verify entered account details of the beneficiary prior to the actual transfer. The verification is based on the unique combination of the account holder’s name information belonging to a specific account number. The payer’s bank sends the entered account name and number to SurePay, which in turn verifies the details against the available data in order to provide a response. Should entered details be incorrect (i.e. the beneficiary name does not match with the names known at the bank for this account number), then the payment initiator will get a notification. The payer might be at risk of payment fraud or possibly has made a mistake.

Verification Of Payee is tailored for the EU market and the SurePay Confirmation of Payee adheres to UK market requirements, rules and regulations.

No, you don’t. SurePay’s Verification Of Payee service is not a separate app, nor programme. Your own bank can opt to integrate SurePay’s Account Name Verification service in its online environment, and make it available to you. The service generally works for online transfers and is commonly made available through a regular banking application.

Currently, SurePay’s services are available to customers of 250+ EU banks.

At the moment, SurePay’s service is available to customers of 250+ banks in the Eurozone and across the UK.

Businesses and organisations can also implement the Verification Of Payee in their own business processes and systems, regardless of what bank they use.

SurePay’s Account Check deploys an intelligent algorithm that compares the user’s entered beneficiary details against the SurePay database, which contains data from several sources such as connected banks and e.g. the Dutch Chambers of Commerce.

The service takes advantage of multiple data fields of the beneficiary’s bank of registry in order to match with users’ input. The outcome can be a match, a near match or a non-match, in which case the user can be prompted with a notification.

For its operations, it is important that SurePay’s service has access to complete and up-to-date client records of connected banks. Ensuring this will help to prevent fraud and payment misdirection.

In order to ensure high quality matching, the SurePay algorithm needs access to the verified customer data of the bank that has issued the account. For business accounts, SurePay retrieves additional trade names as registered at the Chambers of Commerce, for the registry number that the banks hold in their files for their business customers. This is important because payments to trade names should not lead to a warning notification.

SurePay closes agreements with connected banks for the provisioning of customer data, in which purpose limitation is included and clearly described. Meaning that the data you provision as a bank will strictly and solely be used for the agreed purposes.

We deliver a quotation based on your needs, and therefore refrain from stating exact rates. We do, however, provide further information on how our prices are set and what they’re based on.

For banks, prices are roughly built up of a one-off connection fee and a per-call fee to our API, which is based on the aggregate number of transactions over a period of time. For banks who provision their data as well as consume our API, there are significant price reductions available. Please contact an account manager for further enquiries.

Yes. The EPC has provided a Rulebook for API scheme for VOP request to be used between API’s.

- The BIC of the requesting PSP

- The reference of the VOP request from the requesting PSP

- The reference of the VOP request from the requestor

- The result of the VOP request on the account number and name verification. This will be a No Match, Close Match, or a Match.

- In the case of a close match, a name suggestion (corrected name) will be sent.

- The result of the VOP request on the account number and ID verification (this can include multiple results and is optional).

As SurePay, we ensure no data is shared with requesting PSPs that weren’t already known. We take great pride in designing our product with a privacy-by-design mindset and complying with the GDPR.

We have a range of solutions available, ranging from minimal impact to solutions that are ready for scale and offer additional value and ease of use for customers:

- Using the single check for batches, this solution will be useful for smaller banks.

- Using our Batch Check API, connect to our API and deliver large files with multiple VOP requests in one go.

- Integrate our (white-labelled) portal into your online transaction channel and offer your customers the ability to perform file checks.

- After initial checks done by your customers, we also offer an alerting service in case something has changed (account inactive, name changed, switched), adding additional comfort for your customers. While not a compliant solution on its own, it does offer benefits for your customers to rest assured their administration is up-to-date.

→ For a more detailed explanation, refer to the article via this link: Verification Of Payee for Batches

Banks need to sign an adherence agreement with the EPC to become a participant or appoint SurePay to do it on their behalf:

“To apply to become a Participant, an undertaking shall submit to the EPC an executed and original Adherence Agreement and submit Supporting Documentation to the EPC. A Participant may appoint an agent to complete an Adherence Agreement on its behalf.”

The specific moment when PSP’s will be able to become live participants is not known at this time.

Yes, in the case of a Close Match result, the scheme requires a corrected name to be provided. Although not explicitly stated in the Rulebook, it is intended that no data not known to the payer before should be presented.

Quote from the Rulebook:

“The name of the Payment Counterparty as supplied by the Responding PSP back to the Requesting PSP and the Requester in case AT-R001 indicates Close Match. The use of this attribute is limited to Close Match only.”

Note that providing a name suggestion in the case of a close match on a business account is not supported by the Rulebook, contrary to SurePay’s current practice in the case of a no match on a business account.

→ For a more detailed explanation, refer to the article via this link: Solving GDPR Challenges

For PSP’s operating in a euro country, the deadline was October 9, 2025.

For PSP’s operating in a non-euro country, the deadline is July 9, 2027.

The EPC provides a directory service that allows fetching the reachability details of each participant. SurePay ensures reachability by connecting to all available participants. These participants may operate within the same country with different vendors, similar to the situation in the UK, or between countries.

Choosing a provider with a proven solution offers several benefits over building a solution yourself or choosing a vendor with no experience in the field:

Optimised Customer Experience: Perfecting match rates takes time and multiple iterations. This is crucial for a positive user experience. False positives or negatives, or a high No-Match rate, might lead to friction in the customer journey or cause customers to ignore warning messages, potentially achieving the opposite of the intended effect.

Quality of Matching: The quality of matching becomes an important factor as a responding PSP. Failing to respond or providing an incorrect response might lead to liability for any resulting damage.

Shorter Implementation Times: Since SurePay specialises in name matching and connecting PSPs to our service, implementation times are shorter and less expensive compared to doing it on your own.

In the UK, we saw different banks building their own solutions with varying outcomes. Some developed solid solutions, while others experienced difficulties and are now looking to replace their solutions with a vendor. This is not a risk when choosing SurePay; we have standardised our implementation process and removed the hassle of maintaining everything.

→ For a more detailed explanation, refer to the article via this link: Verification Of Payee and Liability

The Final Regulatory text can be found here:

Regulation – EU – 2024/886 – EN – EUR-Lex

The Public consultation document set for the VOP Rulebook can be found here:

Public consultation on the Verification Of Payee Scheme Rulebook

New item from the EPC on CoP:

Public consultation on the Verification Of Payee Scheme Rulebook

News item where the RFP is announced for the Directory Service for VOP:

Update on the forthcoming Request for Proposal for the EPC Directory Service

Notifications

Notifications only appear in the payment initiation screen, prior to sending through your payment, and appear right after you have completed the fields of beneficiary name and account number (IBAN). In the background the check is carried out instantly without any noticeable delay.

Notifications only appear should your entered beneficiary details differ from their registration at the relevant bank. When the beneficiary details you’ve entered correspond to the details of the back account holder at the bank of registry, no notification is given. If the entered beneficiary details contain a typo or rather small deviation from the actual registration, you will be prompted a clickable name suggestion.

Should entered account details match the information known at the bank for the relevant account number, generally no notifications are prompted. When this is not the case, you can distinguish three main types of notifications:

Warning

When the entered name does not match with the account information known at the relevant bank by any means – for instance ‘D. Williams’ instead of ‘K. James’ – a warning notification is prompted. Please be aware that you might be subject to a scam, fraud or may have made a mistake. The notification will tell you that the account holder is registered under a different name at the relevant bank. Consider alternative measures or get in touch with the beneficiary before proceeding to transfer any funds.

Name Suggestion

In case of minor errors, such as a typo, you will be prompted with a suggested name as registered at the relevant bank. For instance, ‘Williams’ instead of ‘Wiliams’. Please check whether the suggested name belongs to the person/company you are intending to transfer funds to.

Service Not Available

SurePay verifies account numbers and their information across its base. In case SurePay is not able to verify account details against an account number, you will be notified as well. This can, for instance, occur for foreign bank accounts numbers for which SurePay may have insufficient information available.

In case you are not able to further verify the beneficiary details in your online banking environment, please contact the beneficiary to cross check the account details. You are responsible for the payments and transfers you make – even when a notification is prompted.

User Experience

The user has always been at the centre of what we do. In designing and building SurePay’s Account Name Verification service we have considered the fact that end-users would always like an uninterrupted and pleasant payment experience. Hence, the check is performed instantly and highly reliable. Moreover, the user always remains in charge. Meaning that regardless of any notification prompted, the user may always choose to continue the transfer.

In line with strict policies and regulations, we never disclose any personal information on private bank accounts in our notifications, unless we’re certain that the user has made a typo when entering the beneficiary details.

Our Account Name Verification solution has undergone thorough testing by thousands of users. This has allowed us to bring to market an even better version of our service right away.

In principle, the user experience (UX) will remain the same. PSP’s are free to display a message they deem appropriate based on a Match, No Match, or Close Match result. SurePay is always ready to assist with suggestions for effective, validated messages.

One area where impact can be expected is the processing speed. Currently, SurePay has a maximum processing time of 500MS (time-out). In the new VOP Rulebook, the maximum processing time is 3 seconds, with the majority of transactions processed in under 1 second.

Start today. Be sure who you pay.