Understanding IBAN-Name Check: What It Is and Why It Matters

With payment fraud on the rise and financial errors costing millions annually, ensuring secure and accurate transactions has never been more important. While the names may vary—IBAN-Name Check, Verification Of Payee (VOP), or Confirmation Of Payee (COP)—they all serve the same critical purpose: verifying account information before payments are processed.

As the adoption of real-time payments grows and regulations like the EU Instant Payments Regulation (IPR) take hold, these verification tools are no longer optional. They are essential for safeguarding trust in the financial ecosystem and ensuring secure transactions.

In this blog, we’ll explain how IBAN-Name Check works, how it aligns with its counterparts like VOP and CoP, and why implementing this technology is crucial for today’s payment systems.

What is IBAN-Name Check?

The IBAN (International Bank Account Number) is a unique identifier used in international and domestic bank transfers, ensuring accurate routing of payments. However, even with an IBAN, errors or fraud can occur if the account details do not match the intended recipient.

To address this, tools like IBAN-Name Check were developed to verify that the IBAN matches the payee’s name. But here’s the important part: IBAN-Name Check is just one name for the same underlying service. Depending on the market, you might encounter different terms:

- IBAN-Name Check: Widely used in the Netherlands and several other countries.

- Verification Of Payee (VOP): Common in the European Union, driven by compliance with EU regulations.

- Confirmation of Payee (CoP): The UK’s term, reflecting its specific regulatory environment.

While the names differ, the core function remains the same—ensuring the account name matches the IBAN before processing a payment. This additional layer of validation helps prevent payments from being sent to the wrong account, reducing fraud and human errors.

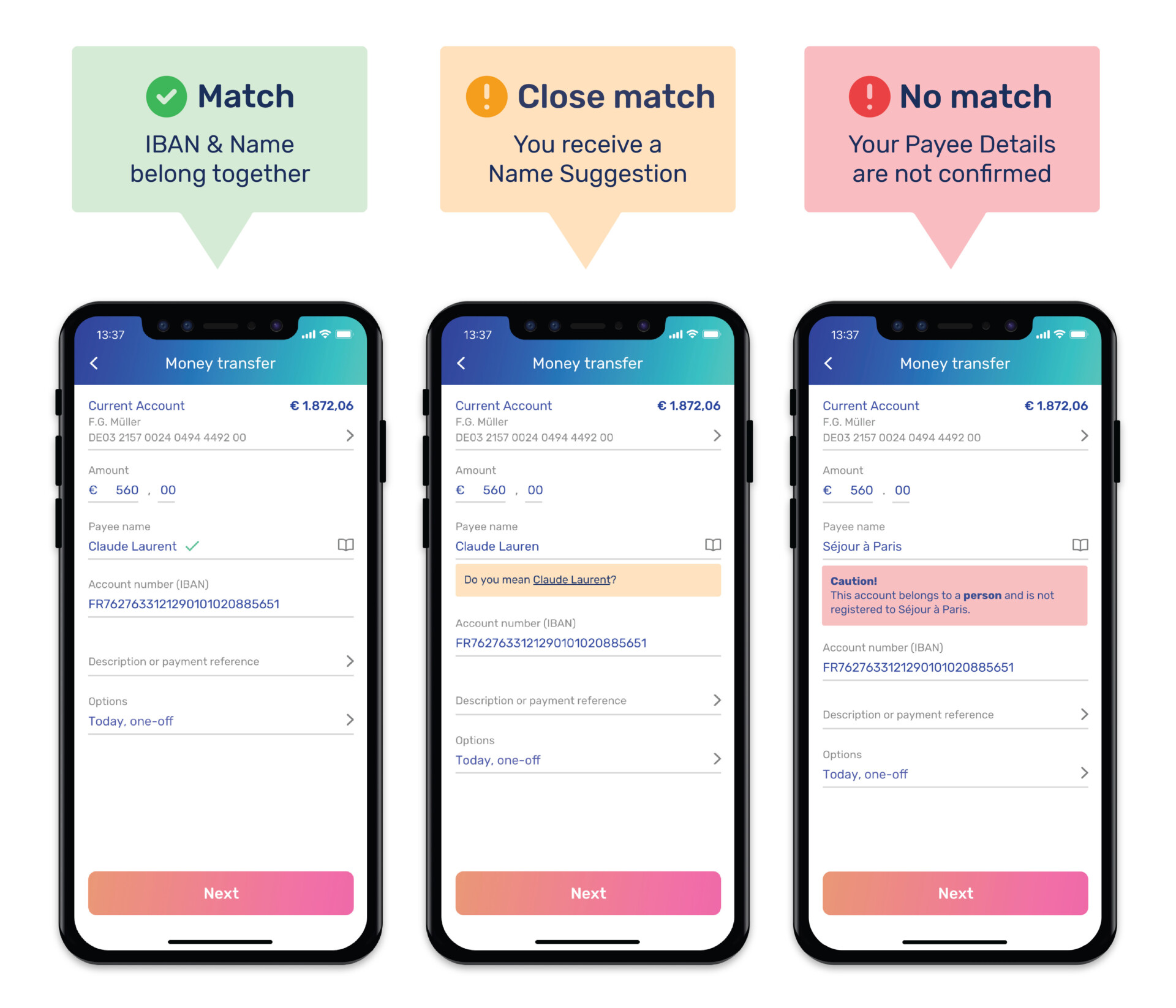

How does the IBAN-Name Check work?

- Cross-referencing information: Matching the provided name with the account holder details linked to the IBAN.

- Flagging discrepancies: If the name and IBAN do not match, the system notifies the payer, indicating the mismatch.

- Providing guidance: Depending on the system’s configuration, it may provide suggestions, such as double-checking the information or contacting the recipient.

This real-time process ensures errors are caught before a transaction is completed, safeguarding funds and reducing the risk of fraud.

Benefits of using an IBAN-Name Check system

For consumers and businesses

- Reduced Risk of Errors: Avoid costly mistakes by ensuring payments are sent to the correct account.

- Fraud Prevention: Protect funds from being sent to fraudulent or incorrect accounts.

- Faster Resolutions: Real-time validation allows issues to be addressed instantly, reducing delays in critical transactions.

For banks and financial institutions

- Minimised Liability: By verifying account details before payments are processed, banks can reduce the financial and reputational risks associated with misdirected funds.

- Cost Savings: Fewer payment disputes and errors mean reduced operational costs.

- Regulatory Compliance: Meets requirements for accuracy and security as mandated by regulations like IPR.

The Instant Payments Regulation: Why IBAN-Name Check Is Essential

The EU Instant Payments Regulation (IPR) is transforming the payments ecosystem, making real-time payments a standard across Europe. IBAN-Name Check plays a pivotal role in achieving the goals of IPR by ensuring transactions are secure, accurate, and compliant.

How IPR Leverages IBAN-Name Check

- Supporting Real-Time Payments: IPR mandates that payments be processed instantly, 24/7. IBAN-Name Check ensures these real-time transactions are accurate, reducing delays caused by errors or fraud.

- Enhancing Security Standards: By requiring tools like IBAN-Name Check and VOP, IPR emphasises the importance of secure payment mechanisms, fostering trust in the financial system.

Meeting Regulatory Requirements

Compliance with IPR means banks must adopt robust verification processes to ensure accuracy and security. IBAN-Name Check is central to this compliance, aligning with the regulation’s goals of fraud prevention, efficiency, and inclusivity. For banks, this means investing in solutions that not only meet these requirements but also streamline operations and improve customer experiences.

Common Questions About IBAN-Name Check

Why are there different names for the same service?

The different names—IBAN-Name Check, VOP, and CoP—reflect the origins of this technology and the markets they serve.

- In the Netherlands: IBAN-Name Check was first introduced to address the specific needs of Dutch banks and payment systems.

- In the EU: Verification Of Payee (VOP) emerged as part of broader regulatory frameworks, such as the EU Instant Payments Regulation, which prioritises accuracy and security in payments.

- In the UK: Confirmation Of Payee (COP) became the standard name as the technology was rolled out to meet local compliance requirements.

How to check bank name from IBAN?

Many online tools and banking systems allow users to input an IBAN and verify its associated bank. These systems cross-reference the IBAN with a database to provide accurate results.

Which banks don’t use IBAN-Name Check?

While most European banks have adopted IBAN-Name Check systems, some regions or smaller institutions may not yet offer this service. It’s best to check with your bank to confirm.

Can IBAN-Name Check be used for foreign accounts?

Yes, but there are limitations. While IBAN-Name Check works well within the SEPA region, it may not be available for accounts outside participating countries due to varying banking standards.

What to do when IBAN-Name Check cannot be executed?

If an IBAN-Name Check fails, double-check the provided details or contact the recipient for confirmation. You may also need to consult your bank for assistance.

Challenges of IBAN-Name Check implementation for banks

Legacy Systems

Many banks rely on outdated infrastructure, making it challenging to integrate modern IBAN-Name Check systems. Upgrading these systems is essential for seamless functionality.

Cost of Implementation

Compliance with regulations and the adoption of IBAN-Name Check tools require significant investment. However, the long-term benefits outweigh the initial costs.

Handling Discrepancies

False positives and minor mismatches, such as typos, can lead to frustration for customers. Advanced systems that differentiate minor errors from genuine issues are essential.

Want to know more about Verification Of Payee?

Best in class Verification Of Payee solution

With our European Verification Of Payee solution, the combination of IBAN & Name will be checked in EU countries, the UK and the world.

Download our whitepaper

Find your answers in our latest whitepaper: “Connecting Europe through Verification Of Payee”

The latest developments

The Digital Euro Is Coming, and Consumers Will Expect to Know Who They’re Paying

There’s something about Canada

6 Things We Took Away from Nacha Smarter Faster Payments

Scammers target Dutch taxpayers as the Belastingdienst bank switch creates new fraud risk

The most important decision in Nordic payments isn’t about the rails.